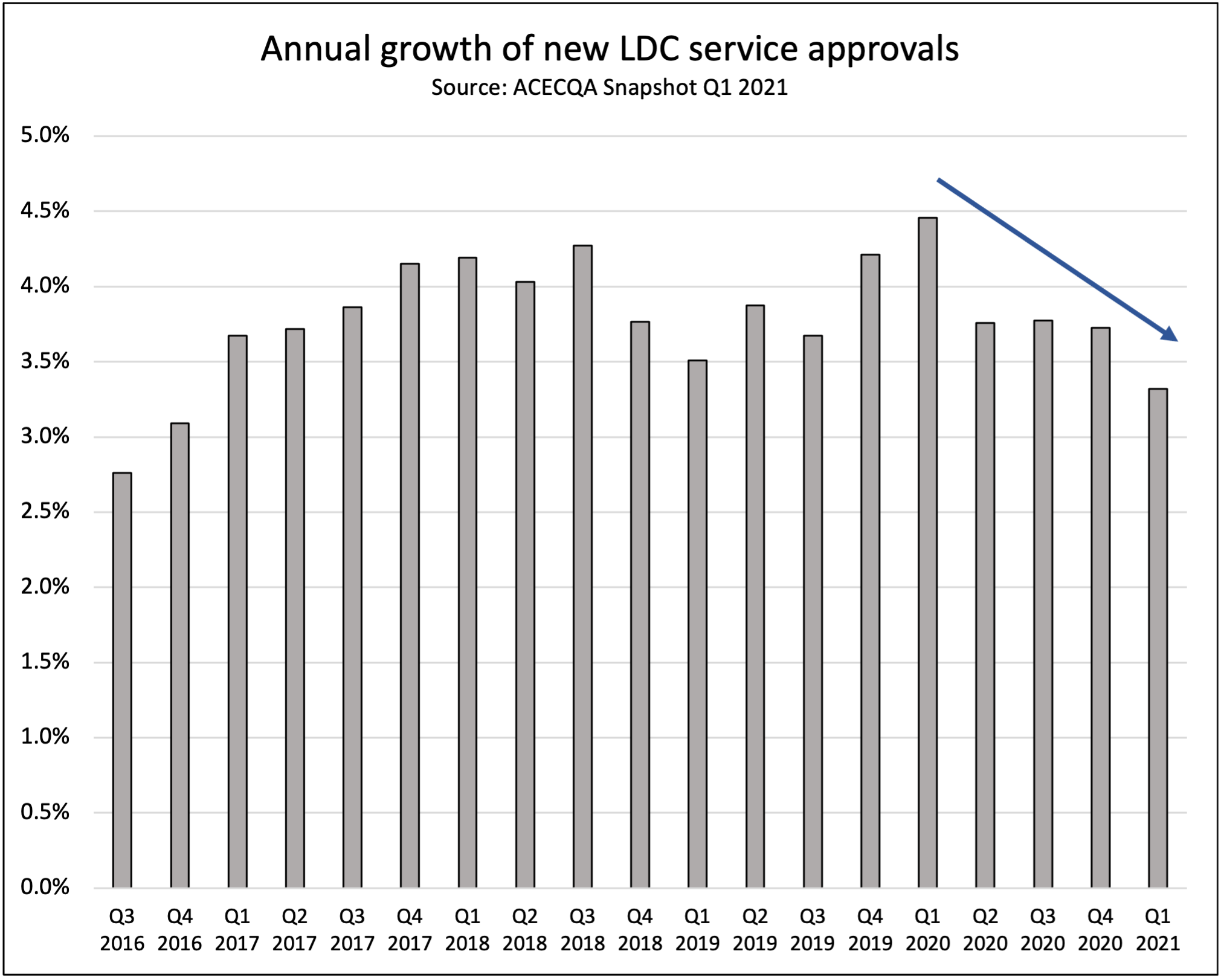

LDC new centre supply steps lower in Q1 2021 as post COVID moderation continues

The growth in supply of new long day care (LDC) centres across Australia has continued to moderate post the onset of the COVID-19 pandemic with the latest Australian Children’s Education and Care Quality Authority (ACECQA) NQF Snapshot reporting a 3.3 per cent increase in centres, the lowest rate since Q1 2017.

The snapshot, which is released quarterly and sources data from the National Quality Agenda IT System (NQA ITS), saw 89 new LDC centres opened in the quarter, substantially lower than the 117 centres recorded in the same period last year.

The ongoing moderation in supply is broadly consistent with indications from the early childhood education and care sector’s two largest REITS, Charter Hall and ARENA, which both reported contractions in their development pipelines, with Charter Hall, in particular, signalling a significant drawdown.

That being said, larger providers such as G8 Education have signalled a resumption in their greenfield pipeline, after a multi year hiatus in pipeline growth, is on the cards in 2021 with ten new centres expected to open.

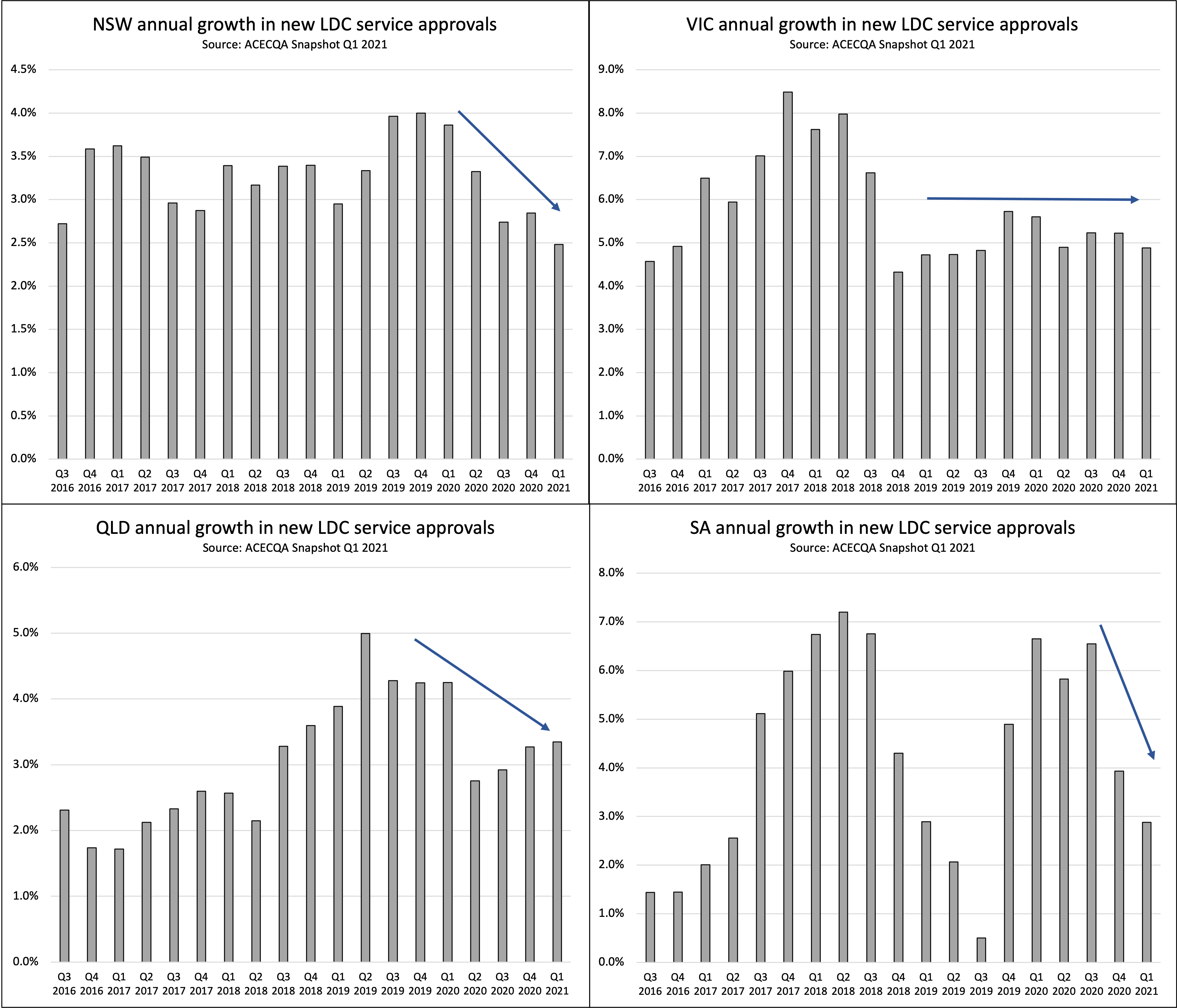

NSW contraction is key driver, although other states also contributing

Across the states and territories of Australia New South Wales appears to be the key driver of the ongoing moderation with a 2.5 per cent annual increase recorded, the lowest since ACECQA started publishing the series.

The reduction in NSW supply is notable given the sharp increase in fees of 3.5 per cent recorded in the broader Sydney metropolitan area in the Q1 2021 Consumer Price Index data released by the ABS which perhaps reflects the market responding to a more favourable supply / demand dynamic and actively pricing accordingly.

Across the other key states on the east coast, and in Western Australia also reported either stable or falling new LDC centre supply.

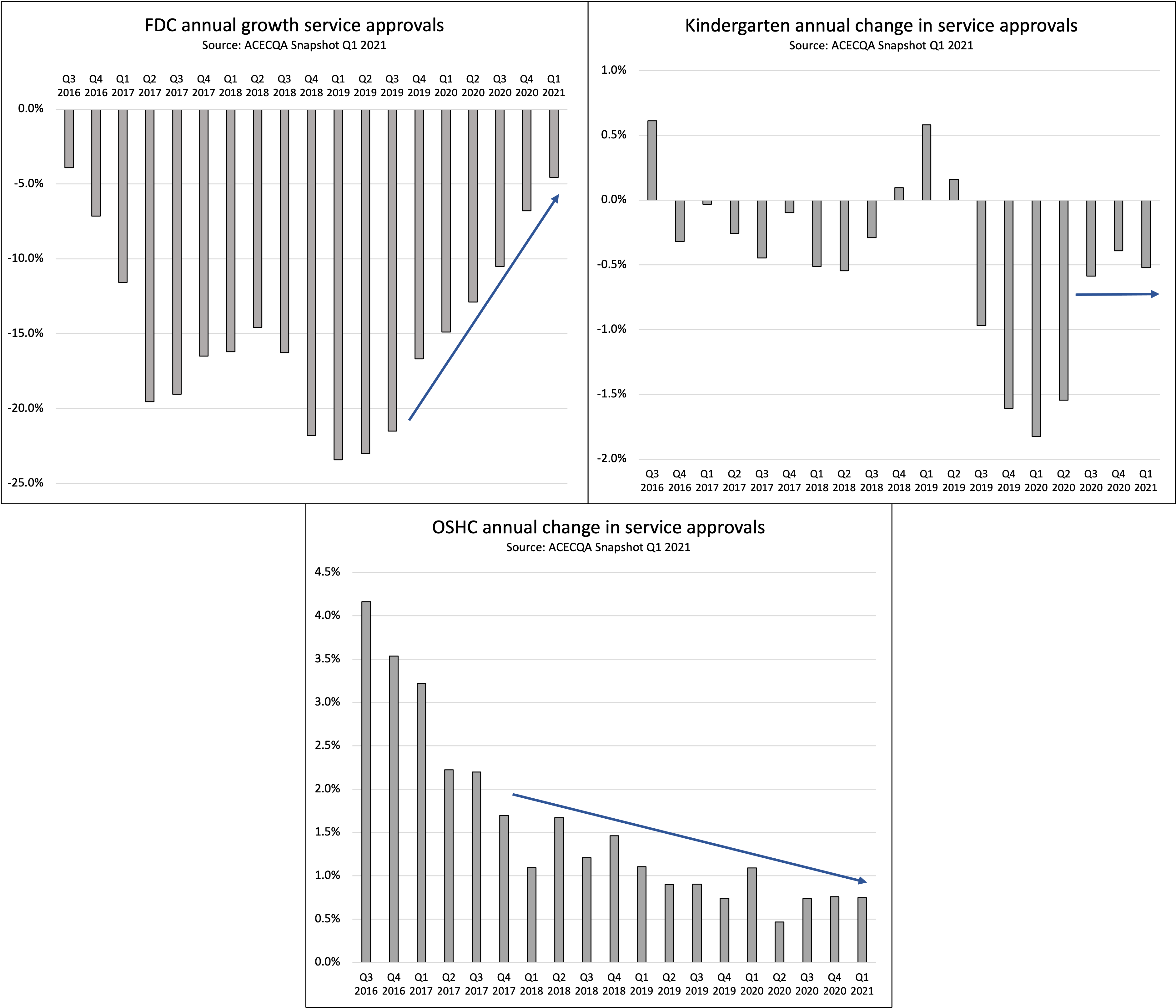

Family day care contraction continues to stabilise, OSHC and Kinder steady

Across the other ECEC settings family day care (FDC) is the most striking having recorded another quarter where the rate of closures continued to moderate from the peaks recorded at the height of the FDC rort related crackdown in mid 2019.

With respect to Kindergarten and Outside School Hours Care, growth levels are broadly consistent with previous quarters with kindergarten showing some moderation in contraction and OSHC maintaining a multi year trend of gradually reducing supply growth.

To read the latest ACECQA snapshot please click here.

Download The Sector's new App!

ECEC news, jobs, events and more anytime, anywhere.

Latest in Economics

Provider

Economics

Police investigate suspicious fire at Turramurra childcare centre

2025-07-11 08:04:41

by Fiona Alston

Economics

Provider

Childcare property market strengthens as investor demand grows

2025-07-10 11:28:25

by Fiona Alston

Economics

Policy

Practice

Provider

Quality

Workforce

CCTV installation to expand across G8 services amid safeguarding concerns

2025-07-09 10:55:31

by Fiona Alston

Popular

Practice

Provider

Quality

Research

Workforce

New activity booklet supports everyday conversations to keep children safe

2025-07-10 09:00:16

by Fiona Alston

Quality

Practice

Provider

Workforce

Reclaiming Joy: Why connection, curiosity and care still matter in early childhood education

2025-07-09 10:00:07

by Fiona Alston

Quality

Practice

Provider

Research

Workforce

Honouring the quiet magic of early childhood

2025-07-11 09:15:00

by Fiona Alston